PAKISTAN GENERAL INSURANCE UNDERWRITING CYCLE

In the mid-1970s & 1980s, the United States found itself in the midst of The Medical Malpractice Insurance Crisis. Malpractice premiums spiked first in the mid-1970s and then again in the mid-1980s. This became a recurring cycle until in some areas, premiums escalated to unaffordable levels. With physicians unable to afford malpractice insurance & a lack of profitability forcing many insurers out of the market, the medical malpractice insurance market was in disarray. The government finally intervened by capping medical malpractice awards and legal reform making it harder to sue. This was ultimately followed by reduced losses and moderated premiums.

Illustrated above is a classic example of the “Underwriting Cycle” – fluctuations in the insurance business over a period of time due to the ebb & flow of business between hard and soft insurance markets. Soft markets are characterized by falling premiums leading to higher insolvency rates among insurers while hard markets tend to be associated with increasing premiums. Managing the underwriting cycle is a challenge for insurers. In 2006, Lloyd’s of London identified the latter as the top challenge facing the Insurance Industry. This article will discuss underwriting cycle of the General insurance sector of Pakistan.

The following graphic shows the underwriting cycle as it manifests in the Insurance market. The starting point of the cycle is arbitrary. Different lines of businesses within Insurance & Reinsurance can be in different stages within the cycle at any single point in time.

What Causes the Cycle

Traditional explanations of the cycle are rooted in classical demand-supply economics. The intricate interplay of supply & price of insurance leads to the hard & soft market that gives birth to each cycle. The demand-supply itself may be driven by political, economic or regulatory factors. It may also be an interplay of all three as in the case of the Medical Malpractice crisis in the United States. An underwriting cycle may also be preceded or succeeded by a Reinsurance cycle.

More recent studies have also focused on behavioral theories that give impetus to the cycle. For example, a study conducted in 2004 talks about the role of short-term compensation structures driving the cycle due to the disconnect between incentives provided to underwriters and the long-term interest of the insurer. Therefore, while major economic or political events may lead to the occasional peaks and troughs in profitability, the behavior of brokers, underwriters & actuaries also plays its own part in fueling the cycle at a micro level.

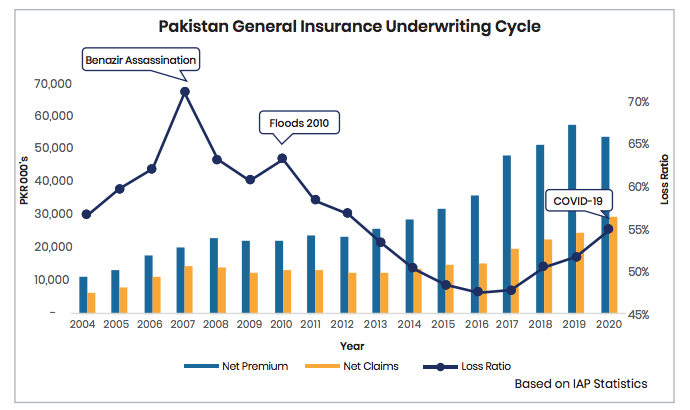

The Underwriting Cycle Of Pakistan

The General Insurance sector in Pakistan is no stranger to the ebbs and flow of the Insurance Market. Indicated by loss ratios in the following chart, the market has witnessed frequent swings in profitability over the period 2004-2020.

The beginning of the review period (2004) is characterized by low loss ratios. From a regulatory point of view, the first set of Insurance Rules in 2002 which brought higher paid-up capital requirements managed to push many General insurers out of the market. This marked the beginning of a hard market reflected by the lower loss ratios at the beginning of our review period.

Against the backdrop of a profitable insurance market, a steady increase in loss ratios is evident from 2004 till 2006 which rises sharply & peaks in 2007. Benazir Bhutto’s assassination in December 2007 dealt a blow to the economy. Amidst plunging stocks & exchange rate exacerbated by surmounting prices, the insurance industry was also swept in this wave of economic uncertainty marking the beginning of another cycle.

Falling loss ratios following the peak in 2007 can be attributed to the adverse shocks caused by the economic turmoil from Benazir’s death. As per capital shock theories of the underwriting cycle, adverse loss shocks cause markets to harden as insurers became cautious in writing business thereby reducing supply and increasing prices at the same time to recuperate losses. This is evident in the downward movement of loss ratios after 2007.

The peak in loss ratios in 2010 can be attributed to catastrophic floods. In this case it was the agricultural & property losses that drove up loss ratios for insurance companies. The consistent fall in loss ratios till 2016 after the floods is the shock theory in play. This particular cycle ended in 2017.

Following 2017, several developments impacted the insurance industry. In 2017, the revised Insurance Rules increased paid up capital requirements. The year 2018 saw two major developments; Imran Khan’s election to prime minister and Pakistan being grey listed by the Financial Action Task Force. Imran Khan’s election had implications for the overall economy, but the FATF grey listing had direct implications for the Insurance Industry as stringent Anti Money Laundering regulation started posing barriers to policy issuance.

For the current the cycle which began in 2017 losses peaked in 2020 as COVID-19 was in full swing. 2020 was also impacted by large losses in the property & fire segment. This was another shock for the insurance industry that could have driven unprofitable insurers out of the market. However, the need to survive amidst lockdowns ushered in a new era for the insurance industry – Digitalization. This has potentially changed the course of the current cycle.

Looking Ahead

The direction that the current cycle may take is uncertain. Despite huge losses during the pandemic, the rapid digitalization of Insurance has led to remarkable changes in the operational & regulatory landscape of the insurance industry. With the upcoming changes in the Insurance Ordinance 2000 & Insurance Rules 2017, the SECP has paved the way for entry of smaller insurers. As more digital & dedicated micro insurers enter the market, we might see the markets soften at least for the next couple of years. However, all we have is conjecture for now. For a more detailed analysis of the underwriting cycle, it should be analyzed at a more granular level with respect to lines of business as each might be impacted by different developments in the market.

PDF Version